Industry Analysis Report Indias Quick Commerce Sector

Industry Analysis Report: India’s Quick-Commerce Sector

By Harsh Rathi | Focused on Zepto

Executive Summary

India’s quick‑commerce (Q‑commerce) market has leapt from US $0.3 billion in 2022 to US $7.1 billion in FY 2024‑25 and now contributes 20 % of total e‑commerce orders. Consulting firm Kearney projects the grocery sub‑segment alone to triple to ₹1.5–1.7 lakh crore (US $18–20 bn) by 2027. Blinkit currently leads with an estimated 40‑45 % share and 1,301 dark stores, while Zepto has accelerated to a 28 % share, 700+ stores and a US $5 billion valuation (May 2025 secondary round).

Zepto’s imminent IPO window (late 2025–early 2026) coincides with:

- Intensifying dark‑store expansion (Blinkit 2,000; Instamart 1,200; Zepto 1,200 target).

- Rising unit economics pressure – Instamart’s AOV now ₹527 and Blinkit’s GOV run‑rate US $4.4 bn.

- Tighter labour & safety oversight – Karnataka’s 1‑5 % gig‑worker cess and draft national hygiene code for dark stores.

Verdict: Zepto can capture upside by doubling profitable micro‑hubs, monetising loyalty (Zepto Pass), and leveraging data‑driven assortment, but must pre‑empt regulatory costs and maintain burn discipline.

Methodology & Limitations

- Data sources: 50+ recent press releases, financial filings, consulting and VC reports (see References). Priority given to FY 2025 figures published after April 2025.

- Estimations: When multiple figures existed, median values were used; currency converted at ₹83 = US $1.

- Scope: Grocery‑led Q‑commerce; excludes restaurant food delivery.

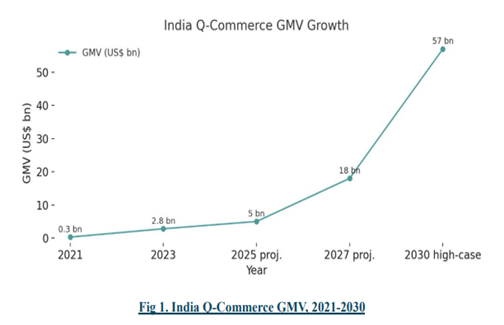

Market Size & Growth Trends

Quick commerce (Q-commerce) is the new, hyper-fast tier of e-commerce, promising delivery of groceries, personal-care items and even small electronics within 10–30 minutes. It relies on dense networks of micro-fulfilment “dark stores,” AI-driven demand forecasting and highly optimised last-mile fleets-technology that lets operators leapfrog the food-delivery model that inspired them and meet rising urban expectations for near-instant gratification.

| Year | GMV (Approx.) | Notes |

| 2021 | US $0.3 bn | Industry in its infancy |

| 2023 | US $2.8 bn | 77 % YoY growth |

| 2025 proj. | US $5 bn | Pace still accelerating |

| 2027 proj. | ₹1.5–1.7 lakh cr (US $18–20 bn) | Expansion to Tier-2/3 cities |

| 2030 proj. | US $35–57 bn | Multiple analyst scenarios |

≈5 × faster growth than traditional e-commerce, signalling a structural shift toward speed-first retail.

What’s Fuelling the Boom

- Convenience culture: Urban Millennials & Gen Z prize instant access, reinforced by 80 %+ smartphone penetration.

- “Forgot-to-buy” baskets: Small, impulsive top-ups fit the 10-minute promise better than weekly bulk trips.

- Pandemic habit-forming: Covid-19 normalised contactless deliveries; behaviour persisted post-lockdown.

- Tech + capital: AI inventory tools, dynamic routing and venture funding sustain deep discounts while scaling dark-store footprints.

Market Dynamics & Friction Points

- Channel cannibalisation: 93% of Q-commerce sales divert spend from kiranas, modern trade and mainstream e-commerce; only 6–8 % is truly new demand.

- Pressure on incumbents: Traditional retailers face falling footfall, margin-crushing price wars and faster inventory obsolescence.

Regulatory spotlight: Alleged FDI breaches (inventory control via preferred sellers) and dark-store zoning issues have triggered government inquiries and could tighten compliance costs.

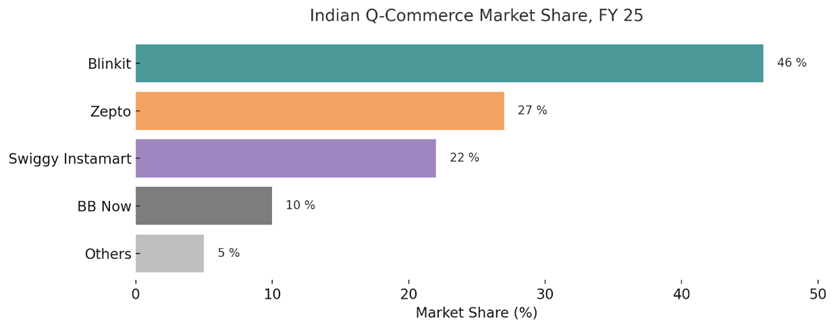

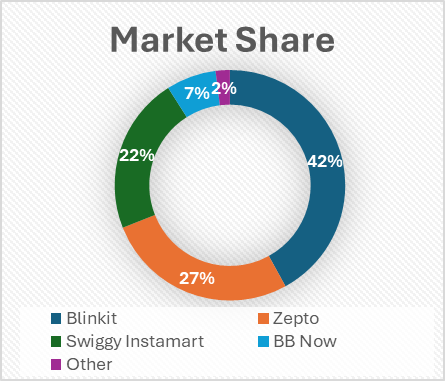

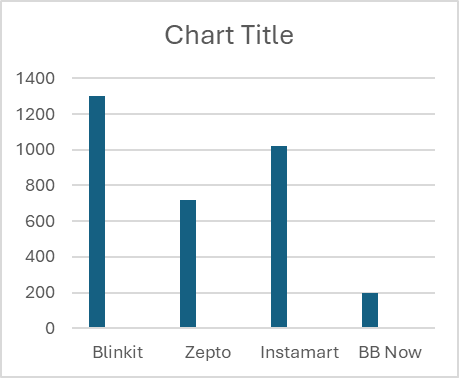

Key Competitors in India’s Quick-Commerce Sector

India’s quick-commerce battlefield is a high-burn, speed-obsessed race in which three heavyweights-Blinkit, Zepto and Swiggy Instamart-control 85% of orders, while traditional e-commerce giants and smaller specialists fight for the rest. Below is a compressed, side-by-side snapshot of who’s winning, how they operate and where they are headed.

Fig 2. Indian Q-Commerce Market Share, FY 25

| Player | Est. Market Share (₹) | Dark Stores (Jun 2025) | FY 2025 GOV Run‑Rate (US $ bn) | Funding / Valuation* |

| Blinkit | 40‑45 % | 1,301 | 4.4 | $568 m buy-out → $13 bn valuation |

| Zepto | 25‑30 % | 720 | 4.0 | $1.9 bn raised; $5 bn valuation |

| Swiggy Instamart | 22‑25 % | 1,046 targets | 3.6 (est.) | Swiggy IPO $1.4 bn; unit profitable goal 2025 |

| BBNow (BigBasket) | 3‑5 % | 200 | 0.4 | Tata invested $7.1 bn across q-commerce |

| Others (Flipkart Minutes, Amazon Now, Dunzo, etc.) | 2‑4 % | n/a | n/a | n/a |

Key insights:

- Blinkit’s scale advantage stems from Zomato cross‑subsidy and deep NCR penetration.

- Zepto’s higher average basket (₹550) offsets a smaller network, enabling clos‑er breakeven per store.

- New entrants (Flipkart, Amazon) will likely erode pricing power in 2026.

Competitive Takeaways

1. Scale vs. Profitability Trade-off.

Blinkit has the volume lead and is edging toward EBITDA break-even.

Zepto and Instamart are chasing top-line growth at similar burn rates, targeting FY26/FY25 profitability respectively.

2. Speed Is Tables takes-Assortment Is the Differentiator

- All top players promise sub-15-minute delivery.

- Winning mind-share now hinges on depth beyond groceries (electronics, fashion, even hot food).

3. Dark-Store Density Decides Unit Economics

- A 1–2 km service radius is the standard; Blinkit and Zepto are pushing towards >2,000 and 700+ stores, locking up premium urban real estate early.

- Capital Still Flows, but Discipline Is Rising

- Mega‐rounds of 2021-22 are giving way to extension rounds tied to concrete profitability milestones.

- Tata, Walmart and Amazon’s entry signals a shift from VC-fuelled land-grab to deep-pocketed conglomerate play.

- Regulatory & Kirana Pushback Loom

- Alleged FDI breaches, zoning for dark stores and kirana cannibalisation could tighten the rules and reshape cost structures.

Consumer-Behaviour Patterns in India’s Quick-Commerce Boom

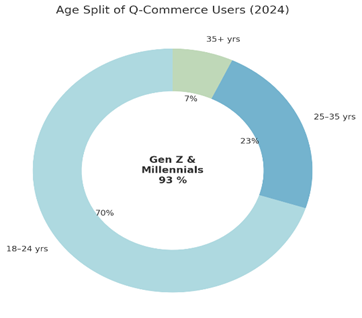

1. Who Buys? – Target Demographics

- Urban, mobile-first Millennials & Gen Z dominate usage.

- 18-24 yrs: >70 % of core users; speed-hungry, app-native.

- 25-35 yrs: most frequent orderers.

- Income & lifestyle: middle- and upper-middle-class households in metros (plus tech corridors of Tier-1/2 cities); time-starved professionals & students willing to pay a convenience premium.

2. How They Buy – Purchasing Habits

- Impulse & top-up culture: ~70 % of orders are unplanned or “forgot-to-buy” refills (snacks, beverages, milk, festive gifts).

- Zepto’s Young Guns cohort: 65 % impulse, 30 % top-up.

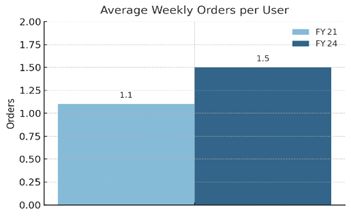

- High cadence: average monthly orders rose from 4.4 (FY21) to ~6 (FY24); 22% of surveyed users open an app daily.

- Typical heavy user: 3-4 orders/week.

- Assortment expectations soar: 7 k+ SKUs per dark store, growing demand for organic, premium and private labels. Players now add fashion, electronics, small appliances.

- Channel cannibalisation: 93 % of

Q-Commerce spend shifts from kiranas, modern trade & mainstream e-com; just 6-8 % is new demand. Nearly half of users cut kirana visits, moving ≥25 % of spend online.

3. What Keeps Them Coming Back – Satisfaction & Retention Drivers

- Speed consistency: ≤ 30 min delivery is the make-or-break metric; users forgive price, not delays.

- Product integrity: fresh, undamaged items; zero “missing SKU” errors.

- Seamless UX: slick app flows from browse → pay in <60 s.

- Responsive support: instant chat refunds build trust after hiccups.

- Smart packaging: no leaks, no odour transfer-vital for perishables.

- Reliability halo: repeat accuracy cements habit and word-of-mouth.

4. Retention Playbook

| Lever | Real-world Example | Outcome |

| Paid loyalty | Zepto Pass hit 1 m sign-ups in 7 days | 3× higher repeat rate |

| AI personalisation | Location-aware promos, “buy again” stacks | ↑ AOV & basket mix |

| Targeted deals | Flash coupons during IPL finals | Surge demand without blanket discounting |

| Consistent CX | Dark-store audits + rider NPS tracking | Fewer support tickets, stronger LTV |

5. Price–Value Equation

- Discount lite: Typical net discount 6–9 %, vs.13–18 % in legacy e-com; delivery fees keep offers sustainable.

- Convenience premium: Urban shoppers increasingly pay ₹15-35 per order for the time saved; willingness rises with income.

- Shift to “quality of growth”: Swiggy, Zepto now dial back deep discounts, aiming for higher spend per retained user rather than pure user-count grabs.

Key Takeaways for Strategists

- Speed is table-stakes―experience is moat. Compete on flawless execution, not just 10-minute pledges.

- Impulse fuels volumes, but trust fuels margins. Nail product accuracy and packaging to curb costly returns.

- Loyalty schemes beat blanket discounts in CAC/LTV math. Paid passes and hyper-personalised offers lock in the most valuable cohorts.

- Kirana dislocation is real; regulators are watching. Smooth community-retail partnerships-or brace for policy heat.

- 20 % of Indian e‑commerce orders now flow through Q‑commerce.

- Gen Z & millennials (ages 18‑35) make up 70 % of users; they cite speed and impulse cravings as top triggers.

- AOVs vary: Instamart ₹527 (Q4 FY25) vs. Zepto ₹550 (company data).

- Late‑Night Snacker and Busy Parent segments remain the fastest‑growing micro‑niches (see Appendix B for personas).

Digital-Marketing Snapshot of India’s Quick-Commerce Sector

Why digital dominates: The core audience-urban Gen Z & Millennials-lives on phones. Post-COVID habits plus 850 M+ smartphones make online channels the only efficient way to acquire, convert and retain buyers who expect instant gratification.

1 | End-to-end digital playbook

- Digital-first, not digital-too: Performance media, social content and CRM pipelines jointly drive acquisition → engagement → repeat orders.

- Real-time loop: Order data flows straight into targeting engines, letting platforms iterate creative and spend daily.

2 | Brand voice & USP

- One-line promises (“Groceries in 10 min”) headline every asset-app banners, search ads, Insta bios-because speed is the category’s master trigger.

- Messaging pillars: Convenience • Speed • Reliability.

3 | AI-fuelled precision

- Ops optimisation: AI routes riders, predicts stock-outs, trims delivery ETAs.

- Marketing personalisation: Browsing + purchase signals feed look-alike models, product recs and time-of-day push alerts.

- Data monetisation: Zepto’s Trade Desk tie-up sells anonymised intent data across CTV, audio and web inventory.

4 | Mobile-first UX

- Apps > 90 % of orders; UI built for one-hand scroll → tap → pay in < 60 s.

- QR / UPI wallets satisfy Gen Z’s need for “tap-and-go” payments.

5 | Channel mix at a glance

| Channel | Core Tactics | Why It Works |

| SEO / Local SEO | “Grocery delivery near me” pages, schema markup | Captures high-intent searches within 3 km radius |

| Paid Ads (PPC) | Geo-fenced Google & Meta campaigns, burst spend during match nights | Instant reach, controllable CAC |

| Social media | Meme posts, creator recipes, Reels/Shorts | Low-cost virality, Gen Z resonance |

| Influencers | Micro-creators for haul & recipe demos | Trust + authentic endorsements |

| Email / Push | Cart-recovery flows, time-slot nudges | Lifts repeat rate, lowers churn |

| Loyalty | Paid passes (e.g., Zepto Pass) & tiered points | Converts deal-hunters to sticky users |

6 | Pricing & ROI reality

- Typical net discount 6–9 % vs. 13–18 % in legacy e-com; delivery fees recoup margin.

- With cash-burn pressure, leaders now chase “quality of growth”-higher spend per loyal user beats top-line vanity.

Regulatory & Compliance Landscape

Quick commerce’s break-neck expansion has crashed into a thicket of Indian rules on capital, labour, food safety and sustainability. Surviving the next phase means solving for cash discipline and policy scrutiny at the same time.

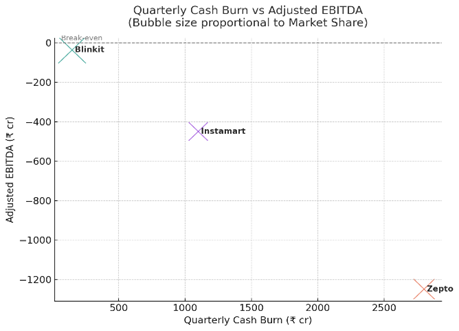

1 | Profitability vs. Cash Burn

- Dark stores + last-mile fleets make the model capital-hungry; the sector reportedly torches ₹5,000 cr every quarter.

- Zepto: FY 24 loss ₹1,249 cr, still >½ of industry burn but targeting PAT break-even by FY 26.

- Blinkit: adj. EBITDA loss trimmed to ₹37 cr (Q4 FY 24) by throttling discounts.

- Deep-pocketed balance sheets, not just speed, decide who lasts.

2 | Foreign-Investment Grey Zones

- FDI law bars foreign-funded e-marketplaces from owning inventory.

- Platforms Park stock in “separate” entities-regulators now probing these structures after trader bodies (CAIT, AICPDF) cried foul.

- Zomato has moved to cap foreign shareholding at 49.5 % for “Indian-owned” status; Zepto eyes a similar rejig.

3 | Gig-Labour Pressures

- 10-minute pledges push riders to risky speeds; take-home pay often ₹10–15 per drop.

- Classed as contractors, couriers lack health cover, PF or paid leave-unions demand fair wages, insurance and algorithmic transparency.

4 | Environment & Sustainability

- Frequent micro-orders raise per-item carbon and plastic use.

- Responses: EV fleet pledges (Zomato → 100 % EVs by 2030), reusable or paper packaging tests, route-batching software.

5 | Infrastructure Hurdles

- Tier-2/3 rollout faces lower basket values and patchy cold-chain; BigBasket alone may need 12–15 m sq ft extra warehousing.

- Prime urban real estate for micro-fulfilment is scarce and pricey; traffic congestion erodes delivery-time promises.

6 | Food Safety & Store Hygiene

- FDA/FSSAI spot-checks have found mould, odour transfer and expired stock; Zepto’s Dharavi hub briefly lost its licence.

- Brands now audit dark stores, segregate food/non-food SKUs and embed IoT temp sensors to pre-empt shutdowns.

Bottom line: Fast grocery must now be fast + compliant-balancing lightning delivery with sustainable unit economics, lawful FDI structures, protected workers and spotless food-safety audits.

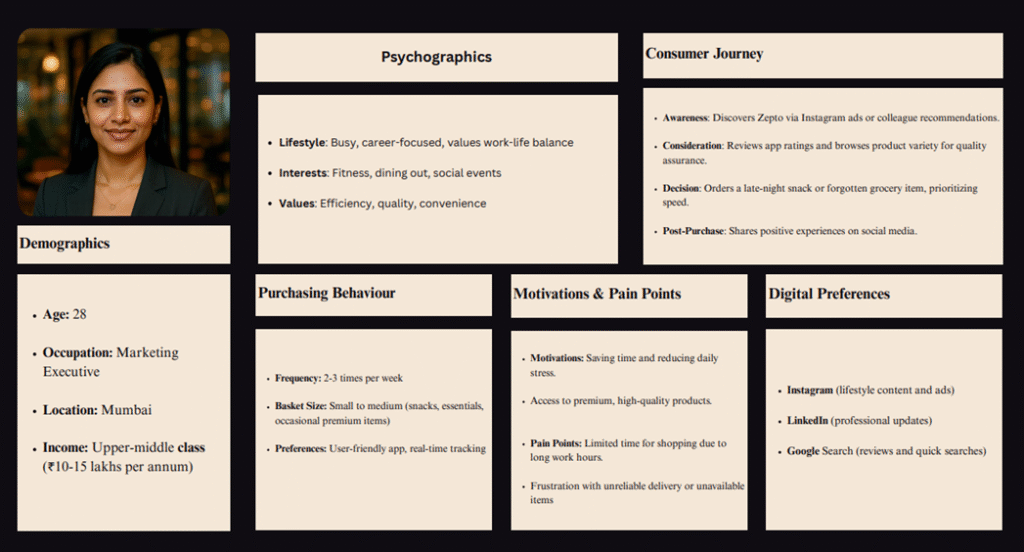

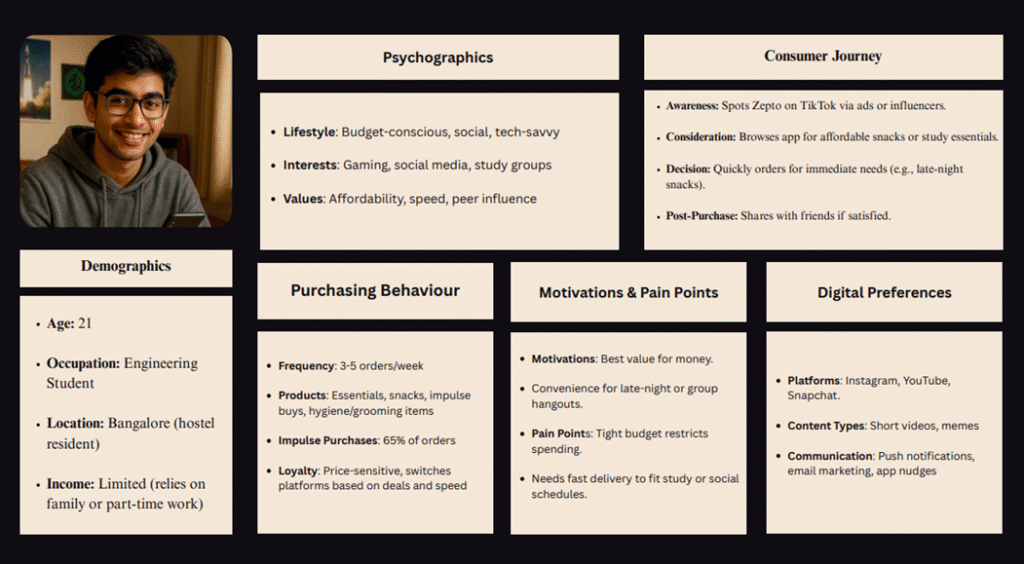

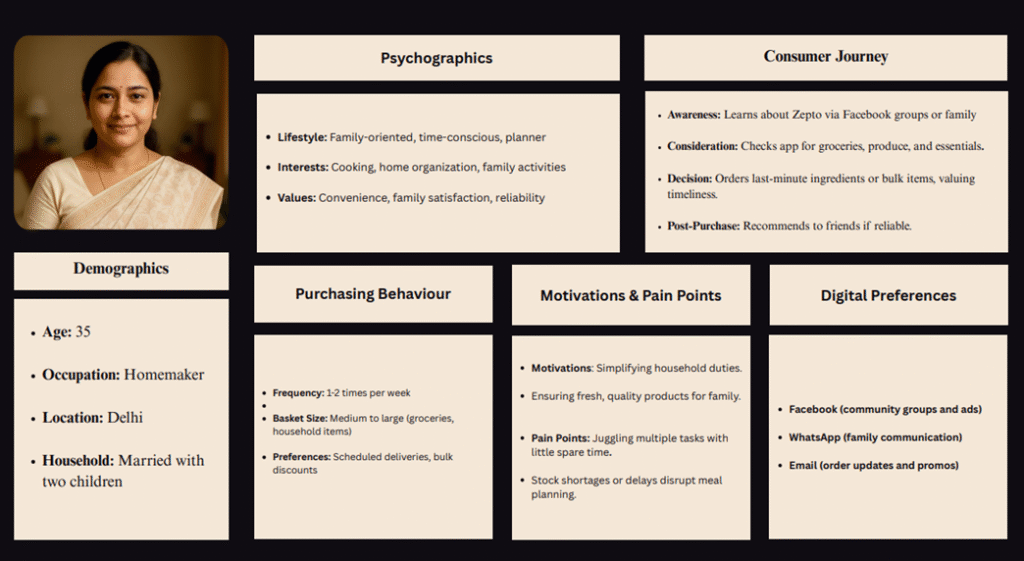

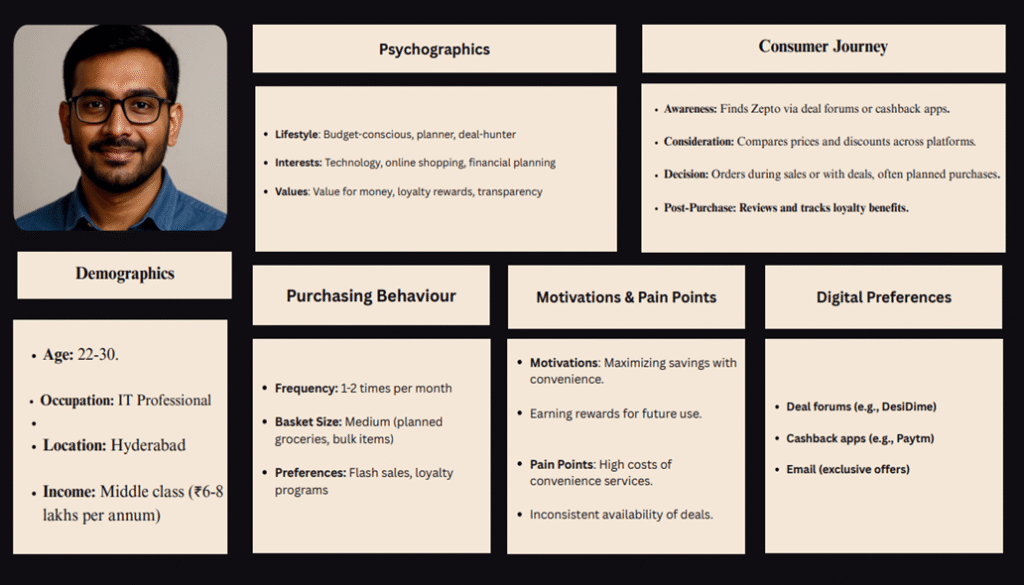

Target Audience Personas

1. Priya the Professional

2. Rahul the Student

3. Anita the Homemaker

4. Vikram the Value Seeker

All persona in High Quality (Click Here)

Competitive Intelligence Dashboard: Zepto

Introduction

This dashboard provides a snapshot of Zepto’s position in the Indian quick-commerce market as of July 2025. It includes an overview of key competitors, current market trends, and strategic insights to guide Zepto’s growth strategy ahead of its planned IPO.

1. Competitor Landscape

This section outlines Zepto’s main competitors, their market share, operational scale, and financial metrics.

| Competitor | Market Share | Dark Stores | GMV (FY 2025) | Funding/Valuation |

| Blinkit | 40-45% | 1,300 | $4.4 billion | Acquired for $566 million |

| Zepto | 25-30% | 720 | $4.0 billion | $13 billion valuation |

| Swiggy Instamart | 22-25% | 1,040 (target) | $3.6 billion (est) | Swiggy IPO $1.4 bn; unit profitable goal 2025 |

| BigBasket (BBNow) | 3.5-5% | 200 | $0.4 billion | Tata invested $7.1 bn across q-commerce |

| Others | 2.4-4% | N/A | N/A | N/A |

Insights

- Blinkit leads with the largest market share and dark store network.

- Zepto’s higher AOV and strong valuation suggest a premium positioning.

- Swiggy Instamart leverages its parent company’s ecosystem for scale.

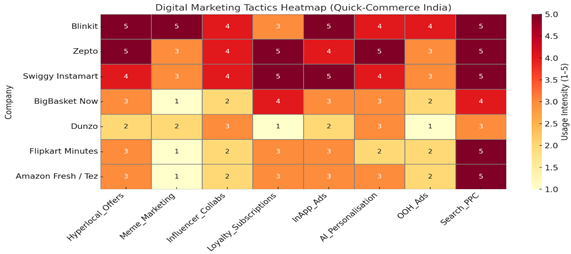

2. Digital Marketing Tactics

This section compares the digital marketing strategies of Zepto and its competitors.

| Competitor | Performance/PPC | Social media & Influencers | Other Tactics |

| Blinkit | High Google Ads spend on “near-me” keywords (5% CTR) | Instagram and Twitter promotions | N/A |

| Zepto | Moderate Google Ads spend | Instagram Reels, micro-influencers (3.2% engagement) | Zepto Pass loyalty program |

| Swiggy Instamart | Low Google Ads spend | Cross-promotion with Swiggy app | In-app notifications |

| BigBasket (BBNow) | Minimal Google Ads spend | Email marketing, loyalty programs | N/A |

Insights

- Blinkit dominates paid search with hyper-local targeting.

- Zepto excels in social media engagement with younger audiences.

- Swiggy Instamart benefits from integrated cross-promotion.

The marketing playbook is mobile-first, targeting a core audience of urban Gen Z and Millennials. While all players use standard tactics like local SEO, PPC ads, and influencer marketing, Zepto has carved out two key advantages:

- Paid Loyalty: The “Zepto Pass” program is a key differentiator, successfully converting deal-hunters into sticky, high-frequency users and driving a 3x higher repeat rate.

- Data Monetization: Zepto has a unique strategy of monetizing its anonymized user data through a partnership, creating an alternative revenue stream.

3. Market Trends

Key trends shaping the quick-commerce sector:

- Market Size: $7.1 billion in FY 2024-25, projected to reach $18-20 billion by 2027.

- Consumer Demographics: 74% millennials (18-35 years old), prioritizing speed and convenience.

- Purchasing Habits: >70% impulse/top-up orders.

- Average Order Value (AOV): Zepto’s AOV is higher (est. $25-30), reflecting premium offerings.

Insights

- Rapid market growth offers expansion opportunities.

- Impulse buying suggests potential for targeted digital campaigns.

4. SWOT Analysis for Zepto

A strategic assessment of Zepto’s market position.

| STRENGTH 10-Minutes DeliveryHigh AOV ₹ 550/-AI-Driven OperationStrong FundingGrowing Brand | OPPORTUNITIES Tier-2 City ExpansionAd MonetisationNew CategoriesNew categoriesESG Branding |

| WEAKNESSES Profitability LagLimited City Count UX GapsGig-Worker Reliance | Threats Intense price warRegulatory ScrutinyReplicable ModelCash-Burn riskSupply Shocks |

Insights

- Zepto can leverage its premium focus and valuation for differentiation.

- Expansion and data utilization are key growth drivers.

- Competition and regulation pose significant risks.

5. Strategic Positioning Opportunities

High-level recommendations for Zepto:

- Premium Positioning: Highlight quality and assortment to justify higher AOV.

- Loyalty Leadership: Enhance Zepto Pass with exclusive perks.

- Assortment Expansion: Add non-grocery categories (e.g., electronics, personal care).

- Financial Discipline: Prioritize sustainable growth for IPO readiness.

Insights

- Differentiation through quality and loyalty can set Zepto apart.

- Financial discipline is critical for long-term success.

Conclusion

Zepto operates in a competitive quick-commerce market dominated by Blinkit and Swiggy Instamart. By leveraging its premium positioning, enhancing loyalty programs, and expanding its assortment, Zepto can strengthen its market position. Addressing its smaller dark store network and maintaining financial discipline will be key to navigating competition and regulatory challenges ahead of its IPO.

Follow me for more: LinkedIn | Instagram | X | Round Table